![]() The Drug Development IPO market enjoyed a strong third quarter, with over $3.18B raised by 26 companies across the globe, bringing the year-to-date total up to 70 IPOs raising over $7.38B. Despite a slowing stream of international companies seeking to list in the US during Q3, the NASDAQ market remains the global epicentre for drug development companies seeking to IPO. APAC exchanges enjoyed a strong Q3 2018, partially due to the recent regulatory changes made by the Hong Kong Stock Exchange to stem the flow of APAC companies listing in the US by allowing pre-revenue drug development companies to raise funds within the region.

The Drug Development IPO market enjoyed a strong third quarter, with over $3.18B raised by 26 companies across the globe, bringing the year-to-date total up to 70 IPOs raising over $7.38B. Despite a slowing stream of international companies seeking to list in the US during Q3, the NASDAQ market remains the global epicentre for drug development companies seeking to IPO. APAC exchanges enjoyed a strong Q3 2018, partially due to the recent regulatory changes made by the Hong Kong Stock Exchange to stem the flow of APAC companies listing in the US by allowing pre-revenue drug development companies to raise funds within the region.

Regional Focus: North America

The NASDAQ continues to dominate, with 18 drug development companies debuting on the market during the third quarter of the year, raising a combined total of over $1.61B with an average IPO value of $89.48M. Historically, we have seen many international companies forego regional markets in favour of raising funds in the US, however all 18 of the companies to IPO on the NASDAQ during Q3 are based in the United States.

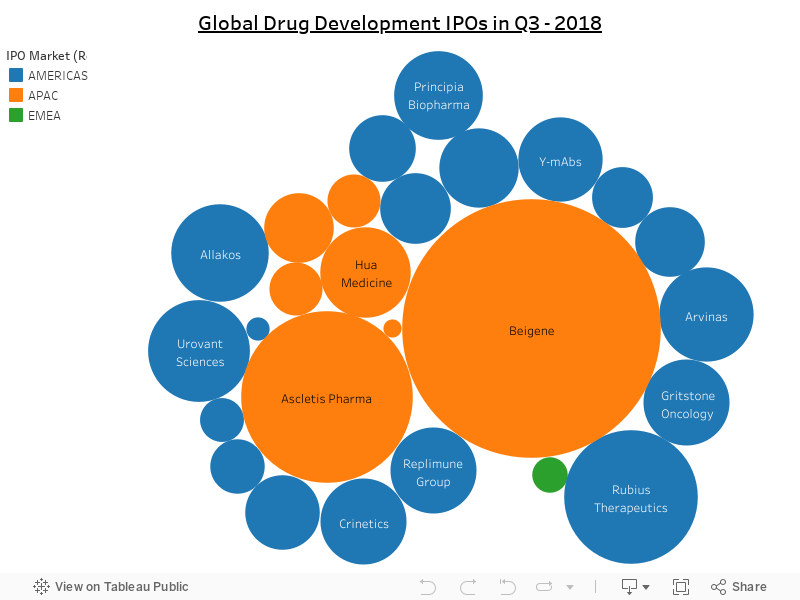

The largest NASDAQ IPO of the quarter was Rubius Therapeutics, which raised $241.1M to support its preclinical pipeline of red cell therapeutics for use in treating rare diseases, cancer and autoimmune diseases. Urovant Sciences raise $140M to support the ongoing phase 3 trials of its lead candidate vibegron, a small molecule drug to treat overactive bladder.

Ten of the 18 companies to IPO on the NASDAQ have an oncology-focused asset in their development pipeline. A trio of American oncology-focused companies IPO’d shortly before the end of the quarter: Arvinas raised $120M for its preclinical pipeline of small molecule therapeutics; Sutro Biopharma raised $85M for its pipeline of ADCs, bispecific antibodies and cytokine derivatives; and immunotherapy-focused company Gritstone Oncology raised $100M to fund the IND and early phase trials of its lead candidate GRANITE-001 for solid tumours.

Regional Focus: Asia Pacific

Seven drug development companies IPO’d on Asia Pacific markets in Q3, raising a combined total of over $1.56B with an average IPO value of $222.4M.

The increasing frequency of APAC listings is partially due to regulatory changes on the Hong Kong stock exchange (HKEX), which recently introduced a rule allowing pre-revenue biotech stocks to list on the exchange. Prior to this change, APAC-based pre-revenue biotechs often opted to raise funds through a NASDAQ IPO. The recent regulatory change by HKEX presents pre-revenue biotechs with an alternative path to raise funds, which several companies have already taken advantage of.

Chinese company Ascletis Pharma was the first pre-revenue biotech to take advantage of HKEX’s relaxed listing criteria, raising $397.51M to support its pipeline of Hepatitis C and HIV treatments. The largest APAC IPO of the quarter was Chinese immuno-oncology company BeiGene, which raised $903M through a secondary listing on the Hong Kong stock exchange, having previously raised $158M through a NASDAQ IPO in 2016. BeiGene’s lucrative secondary listing fell below the company’s target of $1B to fund further R&D studies of its pipeline candidates. However, the successful secondary listing highlights that HKEX’s relaxed rules have succeeded in attracting pre-revenue drug developers and secondary listings for APAC companies that have listed internationally.

Elsewhere in APAC, Australian CNS-focused company NeuroScientific Biopharmaceuticals raised $4.45M on the Australian stock exchange. The Korean market for drug development IPOs has started to recover from the Samsung BioLogics’ accounting scandal in May, with three Korean companies successfully listing in Q3: iCure Pharm ($64.85M), OliX Pharmaceuticals ($38M) & Biosolution ($38.5M).

Regional Focus: Europe

In keeping with historical trends, Q3 was extremely quiet for new listings of European drug development companies. The sole therapeutic company to IPO on a European market during Q3 2018 was Swedish company Asarina Pharma, which raised just over $17M to fund the phase II trials of their small molecule drug for premenstrual dysphoric disorder.

Conclusions

The drug development IPO market has continued to build on the momentum from a strong Q2. Thus far in 2018, 70 drug development companies have IPO’d across ten global exchanges, raising a combined total of over $7.38B with an average IPO value of $105.42M. The $7.38B raised 2018 YTD already exceeds the total amount raised in all of 2017, during which 74 companies raised a combined total of $7.28B with an average IPO value of $98.35M.

As a result of relaxed HKEX regulations, it is expected that the trend of APAC-based companies listing on the NASDAQ market will continue to decline during Q4 and throughout 2019. Biospace has reported that more than 10 biotech companies, predominantly Chinese, have announced plans to list on the HKEX, with several companies dropping plans for NASDAQ listings. Two companies that have already announced plans to list on the HKEX are Innovent Biologics and Shanghai Henlius Biotech.

This article is comprised of selected data from Evolution Bioscience’s exclusive Therapeutic IPO Data Visualisation, which has been updated with all drug development IPOs from 2012 until the end of Q3-2018. In the last six years a total of 476 drug development companies have raised over $40.85B, with an average IPO value of $85.81M.

You can view the fully-interactive data visualisation by clicking on the button below:

Follow Evolution Bioscience on LinkedIn to keep up-to-date with news and trends from the biotechnology, biopharmaceutical, medical device and related industries.